Why Directors Should Not Be the Accounts Approval Bottleneck

In many small and mid-sized construction businesses, the director becomes the final checkpoint for almost everything.

A supplier invoice lands in accounts. A subcontractor sends a claim. A purchase order needs approving. A materials cost is over the expected value. A project manager is not sure whether something belongs to the original scope or a variation. The safest answer becomes: send it to the director.

That feels controlled at first. The director knows the jobs, the suppliers, the cash position, and the history behind difficult calls. But if every approval waits for one person, the business is not really controlled. It is queued.

For UK contractors, fit-out firms, refurbishment teams, and subcontractors, that queue can affect payment runs, supplier relationships, month-end reporting, and job costing. The problem is not that directors should be kept out of financial decisions. The problem is that they should only be pulled into the decisions that actually need director judgement.

Why the bottleneck appears

The approval bottleneck usually grows gradually.

At the start, the business is small enough for one person to hold the details in their head. The director remembers which supplier was used, which subcontractor was on site, what was agreed over the phone, and whether a cost looks reasonable. Accounts can ask a quick question and get an answer.

As the business grows, that informal pattern starts to strain:

- More jobs run at the same time.

- Project managers place more orders directly.

- Suppliers send invoices before approvals are complete.

- Subcontractors submit claims with incomplete references.

- Accounts has to chase people across email, WhatsApp, and phone calls.

- Directors are asked to approve costs without the full job context in front of them.

The director is still expected to make the call, but the information needed to make that call is scattered.

Approval is not the same as understanding

A director can approve an invoice quickly and still not have a clean view of what happened.

That matters because approval should answer more than “can we pay this?” A useful approval process should also show whether the cost was expected, whether it belongs to the right job, whether the purchase order was accepted, whether the goods or works were received, and whether there is any commercial issue to recover.

If those checks are missing, approval becomes a workaround. The invoice may move forward, but the business has not improved its control.

The questions often repeat:

- Which job does this invoice belong to?

- Was there a purchase order?

- Who approved the order?

- Has the site confirmed delivery or completion?

- Is the invoice value within the agreed amount?

- Is this part of the original scope, a variation, or a recharge?

- Has this supplier or subcontractor already invoiced part of the same work?

When those answers are not attached to the invoice, the director becomes the search function.

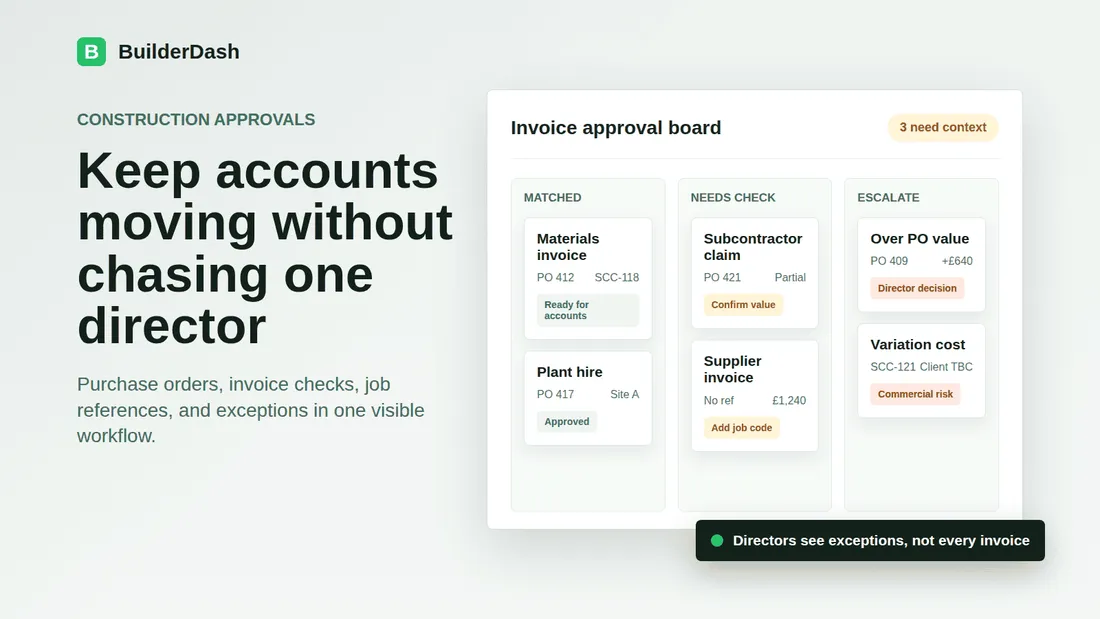

What accounts should be able to check first

Accounts should not have to ask a director basic operational questions on every invoice.

Before an invoice reaches director review, accounts should be able to see the core facts:

- Supplier or subcontractor name.

- Invoice number and date.

- Job code, project reference, or site reference.

- Matching purchase order where one exists.

- Purchase order approval status.

- Expected value and invoice value.

- Delivery note, completion confirmation, or supporting evidence where relevant.

- The person responsible for checking the cost.

That does not mean accounts is making commercial judgement alone. It means accounts can separate routine processing from exceptions.

If the invoice matches the purchase order, the job reference is clear, and the right person has confirmed the cost, it should not need the same level of director attention as an invoice with no PO, no reference, and a value difference.

Where directors should stay involved

Directors still need visibility and authority over higher-risk decisions.

Examples include:

- Unapproved spend above an agreed limit.

- A supplier invoice that exceeds the purchase order.

- A subcontractor claim with a disputed value.

- Costs linked to a variation that has not been agreed with the client.

- Payments that could affect short-term cash flow.

- Repeated exceptions from the same supplier, site, or project manager.

- Any invoice that may expose a margin issue on a live job.

Those are proper director decisions because they involve commercial risk, not just admin delay.

The aim is to make director review more useful. Instead of being asked to approve every routine invoice, the director sees the exceptions that need a decision and the evidence behind them.

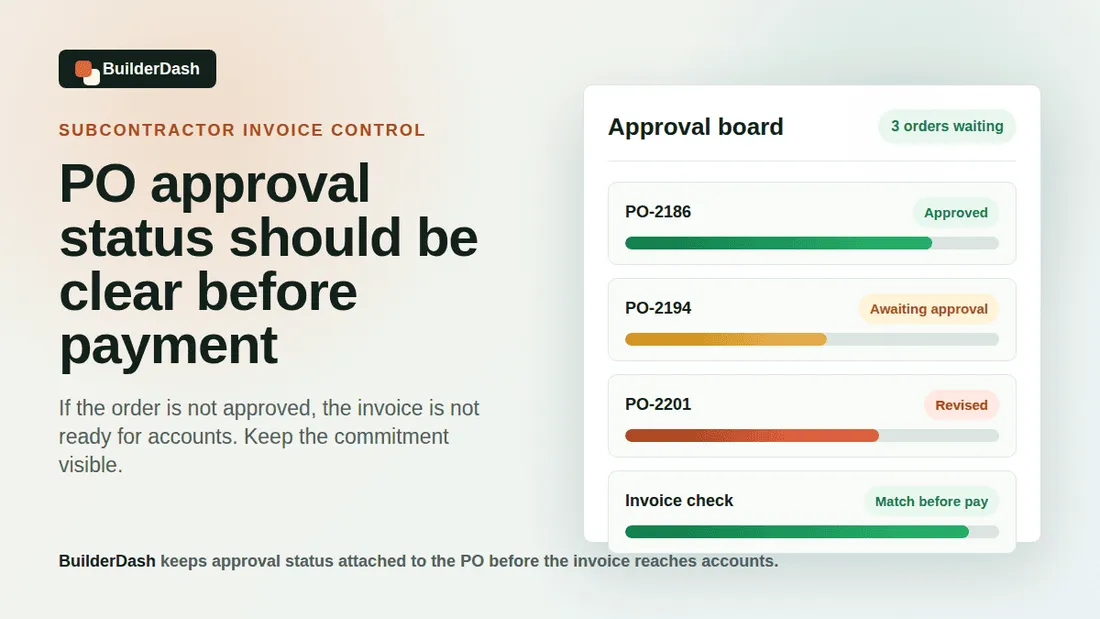

Purchase orders reduce approval noise

Purchase orders help because they move approval earlier in the workflow.

If the purchase order is raised with the supplier, job reference, description, expected value, and approval status, the invoice check becomes easier. Accounts is not starting from a PDF in an inbox. They can check the invoice against what the business already agreed.

A practical purchase order workflow should make these points visible:

- Who requested the order.

- Which job or site the order belongs to.

- Who approved the spend.

- What value was approved.

- Whether the invoice matches the approved order.

- Whether the order has already been partly invoiced.

That reduces the number of invoices that need director involvement later.

The cash flow problem with slow approvals

Slow invoice approvals do not only irritate accounts. They can distort cash flow planning.

If invoices sit unresolved, the business may not have a clear view of what is due, what is disputed, and what can safely be paid. Supplier statements become harder to reconcile. Subcontractor payment runs take longer to prepare. Directors may think they are protecting cash by holding approvals, while accounts is left without a reliable picture of committed costs.

Late approval can also damage job costing. If costs are not checked and posted promptly, project reports lag behind site reality. By the time a margin issue appears clearly, the project team may have already made further buying decisions.

Fast approval is not the same as loose approval. The point is to make good approvals easier to complete on time.

Standardise the approval route

Contractors do not need a complicated approval structure to improve this.

They need a clear route:

- Routine invoices with matching POs go through accounts and the responsible project person.

- Value differences or missing references are flagged before posting.

- Larger or unusual costs are escalated to a director with the supporting information attached.

- Subcontractor claims are checked against the order, previous claims, and agreed work value.

- Payment decisions are separated from invoice validity checks where needed.

This gives everyone a clearer role. Accounts checks the financial and reference details. Project teams confirm operational reality. Directors handle exceptions and cash decisions.

How BuilderDash helps

BuilderDash helps construction businesses connect purchase orders, approvals, invoice checks, job references, and supporting information in one workflow.

That matters because the approval status is visible before the invoice reaches accounts. The business can see whether a purchase order exists, who approved it, which job it belongs to, and whether the invoice fits the expected value. If something does not match, the exception can be handled directly instead of being buried in an email thread.

BuilderDash does not remove director judgement. It gives directors cleaner information and fewer routine interruptions, so they can focus on the decisions that actually need them.

A practical test for your approval process

Look at the last ten invoices that needed director approval and ask:

- Did each one genuinely need director judgement?

- Was the purchase order visible?

- Was the job or site reference clear?

- Was the value difference obvious?

- Had the project team already confirmed the cost?

- Could accounts see why the invoice was being escalated?

- Was the decision recorded clearly afterwards?

If the answer is no on several of those, the approval process is probably relying too heavily on memory and informal chasing.

Control should not depend on one inbox

Directors should have control over construction spend. They should not have to personally decode every invoice, purchase order query, and subcontractor claim before accounts can move.

A better workflow keeps approvals visible, pushes routine checks to the right people, and escalates the exceptions with context. That gives accounts a cleaner route, gives project teams clearer responsibility, and gives directors a better view of risk.

The result is not less control. It is control that does not depend on one person being available at exactly the right moment.

Related reading: Construction purchase order software, reducing end-of-month invoice chasing, and spotting partial subcontractor invoices.

BuilderDash can help: Use BuilderDash to keep purchase orders, approval status, invoice checks, job references, and escalation decisions visible before costs reach bookkeeping.

Run your projects properly with BuilderDash.

One system for every enquiry, job, quote and invoice — built for project-based trades, not reactive call-outs.